Module 10 – Financed emissions

Understanding financed emissions is the critical first step towards aligning with global best practices, meeting regulatory expectations and preparing business models for a low carbon future. Financed emissions refer to GHGs linked to the loans and investments made by FIs.

To approach calculation and disclosure credibly, even in data-constrained environments, institutions need a clear understanding of the terminology, methodologies and standards that underpin financed emissions.

- GHG emissions – Scope 1, 2 and 3

- Scope 1 (Direct emissions): GHG emissions released directly by an organisation through sources it owns and controls.

- Scope 2 (Indirect energy emissions): emissions from the generation of electricity, steam, heating or cooling purchased and consumed by the organisation.

- Scope 3 (Other indirect emissions): all other emissions that occur across the value chain of the organisation, both upstream and downstream.

- Attribution factor

- The share of a borrower’s emissions that is allotted to the FI, based on the size of its exposure relative to the total value of the client or project. For example, if bank provides a $2 million loan to a $10 million agribusiness – a 20 per cent share of the company’s total capital structure – and the agribusiness emits 4,000 tCO2e per year from its normal business operations, the bank’s financed emissions would be 800 tCO2e per year.

- GHG Protocol

- The foundational global standard for corporate GHG emissions accounting, which underpins the Partnership for Carbon Accounting Financials (PCAF), which builds on the GHG Protocol and is widely referenced by regulators.

- Partnership for Carbon Accounting Financials (PCAF)

- A global initiative that sets the standard for measuring and disclosing the GHG emissions linked to an FI’s loans and investments.

- Covers major asset classes such as business loans, project finance, listed and unlisted equity, commercial real estate, mortgages, vehicle loans and sovereign debt.

- Aligns with the GHG protocol, ensuring financed emissions reporting is internationally consistent and credible.

- Uses a 1-5 data quality scoring system to help FIs transparently track and disclose the reliability of their emissions data. Score transparency is considered best practice as it highlights data limitations, gaps and areas for improvement.

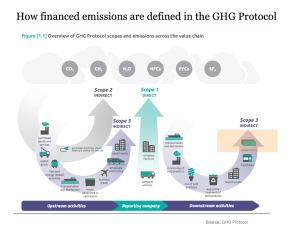

The figure below visualises the range of GHGs covered in the GHG Protocol, and shows how emissions are categorised across Scope 1, Scope 2 and Scope 3 boundaries over time. The orange highlight draws attention to Category 15 of Scope 3 emissions – financed emissions. These are often the most significant yet least visible component of an institution’s overall climate impact, and according to CDP can be up to 700 times larger than an FI’s direct emissions. Measuring Scope 3 emissions can be difficult, so it is acceptable to start with Scope 1 and Scope 2, while developing plans to phase in Scope 3 emissions over time.

Unlike emissions generated from an institution’s own operations, such as office energy use or business travel, financed emissions are indirect. They occur in the real economy through the activities of clients and borrowers whose operations are enabled by the financing they receive from the institution.

- In most cases, an FI’s aggregate Scope 3 financed emissions will outweigh its operational Scope 1 and 2 emissions, by orders of magnitude.

- For example, if the FI lends to a cement manufacturer or invests in a coal-fired power plant, it assumes the responsibility for a proportional share of that company’s emissions, based on the size of the loan relative to the borrower’s total capital structure.

Financed emissions present transition risks and opportunities

Financed emissions are a key transition risk driver for FIs and shape exposure to regulatory change, influence the credibility of an FIs sustainability strategy, and affect its reputation in the shift to a low-carbon economy.

- Materiality for transition risk management Monitoring financed emissions helps FIs to pinpoint where they are most exposed to transition risks such as carbon pricing, emissions regulation, low-carbon technological disruption or changing market preferences for low-carbon alternatives. Any of these factors could affect the long-term viability of an asset.

- Regulatory and disclosure requirements Evolving standards such as IFRS S2 and growing stakeholder expectations can rapidly alter the transition risk profile of an asset at any point of its tenor.

- Reduced portfolio resilience High levels of financed emissions can make institutions more vulnerable to transition shocks, particularly when exposures are concentrated in high-emitting sectors. These risks can lead to asset devaluation, credit deterioration and stranded assets as regulations tighten, ultimately threatening capital strength, lending capacity and long-term portfolio resilience.

Tracking financed emissions can also unlock value creation opportunities for FIs.

- Business Case for tracking financed emissions

Strategic and commercial opportunities

Measuring financed emissions helps FIs to identify carbon-intensive exposures, engage with clients on transition planning, and set risk-based lending limits aligned with organisational risk appetite as well as strategic steering of the portfolio to align with Paris-aligned targets.

Climate finance opportunities

Financed emissions data helps FIs to identify sectors, clients and assets that are well-positioned for transition and adaptation financing. This insight can support the growth of climate-positive portfolios, the design of targeted green and transition products, and access to funding from DFIs and other climate finance investors. Over time, this can strengthen both risk-adjusted returns and the institution’s contribution to real-economy decarbonisation.

Alignment with national/global climate goals

By measuring and managing financed emissions, FIs can demonstrate tangible progress towards global frameworks such as the Paris Agreement and the SDGs. Linking portfolio-level emission profiles to science-based targets or national commitments such as NDCs builds credibility in transition planning.

Enhanced reputation

Transparent tracking of financed emissions signals accountability and leadership to regulators, investors and clients. FIs evidencing active management of their financed emissions can build stakeholder trust, attract top talent and strategic partners, while positioning themselves as leaders in sustainable finance.

FIs can refer to the PCAF Standard for detailed guidance on measuring and reporting financed emissions. PCAF’s globally recognised methodology quantifies portfolio emissions in a consistent and comparable manner, benchmarking across asset classes and meeting best practice disclosure standards.

Guidance 8: Step-by-step guide to calculate financed emissions

Guidance 8a provides a high-level step-by-step approach to calculating financed emissions. It is a conceptual overview of a technical process, and actual financed emissions calculations should be undertaken by verified experts. The GHG Protocol also offers useful guidance and worksheets for calculating cross-sector, sector-specific and country-specific financed emissions.

Guidance 8b demonstrates how financed emissions are calculated for a project where the FI finances only part of the asset’s economic value and is therefore only responsible for a portion of the asset’s emissions. Guidance 8c offers a reference list of industry-standard tools and resources that support detailed financed emissions calculation or validation.

CLICK HERE TO DOWNLOAD GUIDANCE 8: Step-by-step guide to calculate financed emissions

Practical tips to navigate typical challenges associated with financed emissions

Measuring financed emissions can present practical hurdles, particularly where data, methodologies and resources are limited. Common challenges include:

- Lack of available quality data from clients, especially in emerging markets

- Internal resource and capacity constraints, including lack of IT support

- Inconsistent methodologies due to evolving standards and technical assumptions

- Low client awareness or engagement

However, FIs can still take practical steps to prioritise effort, manage uncertainty, and build capability over time.

- Start with material and high impact exposures

- As with transition risk assessment (to which financed emissions are complementary), focus on prioritising sectors and projects with the highest emissions.

- Emphasise transparency over perfection

- Perform the exercise diligently even if data is incomplete, noting gaps as areas for future improvement.

- Treat financed emissions monitoring as a tool for managing transition risk exposure, not as a compliance exercise.

- Be transparent about assumptions, limitations and improvement plans as transparency is appreciated by external stakeholders.

- Leverage external benchmarks and partnerships

- Use credible data providers and sector benchmarks to complement data gaps.

- Collaborate with industry bodies, DFIs or local regulators to get technical assistance where available.

- Build up internal capacity over time

- Start with simple spreadsheet-based tools for high priority clients.

- As resources permit, invest in staff training, IT systems and third-party platforms.

- Engage clients early and constructively

- Frame data requests as part of broader support on client sustainability and resilience.

- Offer clients guidance, templates or technical assistance referrals where helpful.

- Plan for change

- Monitor the regulatory landscape and update internal processes accordingly.