Module 5 – Climate risk appetite statement

Climate risk is a financial risk driver that affects credit quality, asset values and institutional reputation. A climate risk appetite defines the overall level and type of climate-related risk an organisation is prepared to accept in pursuit of its strategic objectives. Quantifying this risk and setting explicit boundaries is foundational for turning climate ambition into robust decision-making. A Risk Appetite Statement (RAS) is a formal, board-approved document that outlines the specific types and levels of risk the organisation is willing to accept or avoid.

A comprehensive approach to developing climate risk appetite development rests on three pillars: clear risk appetite statements, defined materiality thresholds, and well-structured escalation protocols.

- Setting a climate risk appetite

Risk appetite statement

The risk appetite statement aligns the board’s vision for climate risk tolerance with day-to-day operations. It should reflect internal strategic priorities, framing the willingness to accept, mitigate or avoid specific climate-related exposures.

Materiality thresholds

Climate risks vary in importance across institutions. Materiality thresholds translate the overall risk appetite into clear operational limits, by defining which risks require the most attention and resources. They assign financial value to what the institution considers moderate or severe levels of climate-related risk.

Escalation protocols

Escalation protocols act as operational guardrails to ensure that when climate-related exposures exceed risk appetite or materiality thresholds, predefined actions are triggered across the institution’s three lines of defence.

The risk appetite statement sets the overall boundary for an organisation’s climate risk tolerance. Risk limits translate this appetite into practical, actionable triggers for internal engagement, while escalation protocols ensure any breaches feed back into timely responses, learning and ongoing adjustment. Together, this triad of risk appetite, materiality thresholds and escalation protocols forms the foundation of climate resilience for FIs, particularly as climate risks become more acute, interconnected and subject to greater scrutiny by regulators and stakeholders.

The following materials (3a-3d) outline a step-by-step approach to developing a risk appetite statement. These steps highlight key considerations, dimensions and constraints involved in developing a robust risk appetite framework which institutions can adapt and consolidate to fit their own processes.

- Guidances 3a-3d: Risk appetite statement developmentGuidance 3a: Transmission channel narratives

Provides a framework for mapping how climate events in the real economy can result in financial risks for the institution. These narratives help engage relevant teams in understanding and discussing climate risk.

Guidance 3b: Risk appetite statement template

Outlines a methodology for selecting climate risks to include in the risk appetite statement and offers a reference table of contents. A strong statement clarifies the institution’s position on lending to clients exposed to physical or transition risks.

Guidance 3c: Risk limits and materiality thresholds

Explains how to set risk limits and materiality thresholds, providing an operational guide for defining limits on critical hazards affecting the portfolio. These limits support monitoring, internal reporting and the audit of climate risk management.

Guidance 3d: Escalation protocols

Describes how to embed escalation protocols within the organisation and link them to risk monitoring processes.

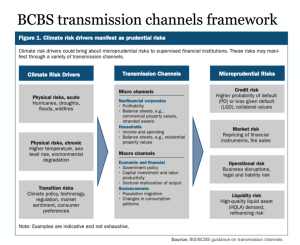

Understanding transmission channels for climate risks

Climate risks are best understood as drivers of existing risk categories, rather than separate risks. The Basel Committee on Banking Supervision (BCBS) transmission channels framework offers a systematic approach to describe how climate risks can materialise as financial risks.

Here are two examples of transmissions channel narratives for tracking the cause-and-effect chain of how climate risks manifest as financial impacts for FIs.

- Example linked to physical riskA period of heavy rainfall causes severe flooding in a major city, disrupting transport networks, damaging prime real estate and triggering major losses for agrifood companies. As a result of, banks in the region face rising credit risk, due to real estate devaluation and mortgage defaults, and operational risks from disrupted banking services and damage to local offices.

- Example linked to transition riskA key trading partner introduces strict carbon pricing, sharply affecting import-export flows between countries. High-emitting sectors face rising costs, which are passed on to consumers reducing demand and slowing industrial output. Companies without credible transition plans also face the risk of stranded assets as valuations fall. As a result, banks experience liquidity pressures on affected corporate bonds and capital outflows from clients in high-emitting industries. Market risk also rises due to collateral repricing across affected portfolio segments.

Guidance 3a: Illustrative examples of transmission channels

Guidance 3a provides a structured framework for developing climate risk transmission channel narratives, helping FIs trace how climate hazards or transition shocks lead to financial risks. They enhance internal risk assessment and scenario analyses, while also supporting clear communication with regulators, investors and stakeholders about how climate risks could affect operations and performance.

CLICK TO VIEW Guidance 3a: Guidance for developing climate risk transmission channel narratives.

Setting a risk appetite

Risk appetite defines the overall level and type of risk an organisation is willing to accept in pursuing its strategic objectives. It is a forward-looking concept that sets clear boundaries for acceptable risk-taking, as approved by senior leadership and the board.

For example, a bank might state it is willing to tolerate a specific percentage of non-performing loans under defined stress conditions. It could also note a low tolerance for operational risks that disrupt services, while remaining open to calculated risks in product or service innovation to strengthen competitiveness.

Risk appetite is ultimately a strategic tool. Its purpose is not simply to limit losses but to guide informed, intentional risk-taking that supports organisational goals. For instance, commercial banks with overly cautious risk appetites may lag in innovation, while MFIs taking too conservative an approach may safeguard loan quality but weaken their mission to expand financial inclusion. Balancing caution with purposeful risk-taking is key to achieving long-term resilience and impact.

A Risk Appetite Statement (RAS) is a formal, board-approved document that clearly defines the types and levels of risk an organisation is prepared to accept or avoid. It outlines the guiding principles, measurable limits and materiality thresholds for the financial risk categories relevant to the institution’s activities.

Two related terms in this context are risk tolerance and risk capacity.

- Risk tolerance Risk tolerance refers to the specific measurable limits – such as maximum allowable losses, limits on exposures or materiality thresholds that trigger escalation – set within the broader, strategic risk appetite. For example, an FI may state it will not tolerate more than $5 million in losses in any business line per quarter.

- Risk capacity Risk capacity is the maximum level of risk an organisation can bear, based on its capital, liquidity and regulatory constraints. It represents the outermost limit beyond which the institution’s viability could be threatened.

An organisation’s risk appetite expresses, in clear terms, the trade-offs between risk and return that senior management is prepared to accept. It should be consistent with portfolio composition, strategic goals and regulatory obligations. Establishing a risk appetite also requires putting in place oversight and risk management mechanisms to monitor limits and thresholds as both a strategic and operational priority.

The following methodology offers a step-by-step approach for choosing climate risks to include in the organisation’s risk appetite.

- Map the organisation’s climate risk landscape

- Develop or apply a taxonomy covering both physical and transition risks, including ‘misalignment’ risks such as stakeholder responses to greenwashing or missing Paris-aligned targets.

- Analyse the climate risk landscape across portfolios, sectors and geographies to identify the largest exposures, and key clients of concern.

- Prioritise the most material climate risks

- Analyse how exposed the portfolio is to climate risks, ideally with granular breakdowns by hazard, sector, geography, and identify the most material risk concentrations.

- Clarify which financial risk categories these exposures relate to, such as credit, liquidity, market or operational risk.

- Align with organisational strategy

- Ensure that all risks included in the risk appetite statement reflect the institution’s climate strategy, business model and regulatory environment.

- Engage the board early to confirm strategic priorities, such as sectoral decarbonisation, financed emissions targets or adaptation goals, and get buy-in.

- Define organisational risk appetite

- Qualitatively, institutions can establish principles-based commitments, for example ‘no new lending to coal sector.’

- Quantitatively, institutions can set measurable thresholds, such as ‘no more than X% of new lending to high-risk flood zones.’

- Consult and refine with internal stakeholders

- Collaborate with risk, sustainability, business lines and internal audit teams to test draft risk appetite statements and confirm that proposed metrics are realistic, while maintaining a suitable level of ambition.

- Engage external stakeholders

- Communicate with an emphasis on transparency, proportionality and a forward-looking, market-responsive approach.

- Present climate risk maturity as a journey, acknowledging the current stage while demonstrating commitment to continuous progress towards more advanced stages.

Guidance 3b: Defining and quantifying risk limits in RAS

Guidance 3b highlights best practices for structuring a risk appetite statement, including its purpose, alignment with strategy and governance, clear articulation of risk appetite, and the use of thresholds for monitoring.

CLICK TO VIEW Guidance 3b. Best practices for developing RAS.

Specifying materiality thresholds for climate risks

Setting materiality thresholds is a critical step in ensuring climate risks are consistently identified and addressed across the organisation. The following approach can be adapted by institutions to suit their specific context, helping to turn climate risk concepts into operational decision boundaries.

- Define the scope and basis for materiality

- Clarify the level at which boundaries will be set – portfolio, sector, geography or client/asset-level – and whether they apply to physical risks, transition risks or both.

- Decide on the assessment criteria, including whether thresholds will focus only on financial materiality, or also consider double materiality (capturing both financial and impact perspectives).

- Align with strategic objectives and risk appetite

- Link thresholds directly to the board-approved risk appetite statement, organisational position and overall climate strategy.

- Engage the board and senior executives early to agree on risk tolerance levels and preferred time horizons.

- Identify key metrics and data sources

- Choose relevant key risk indicators (KRIs), such as:

- Percentage of total assets in high physical risk zones

- Financed greenhouse gas GHG emissions (absolute or relative)

- Sectoral or geographic portfolio concentrations

- Economic capital at risk based on scenario analysis or stress testing

- Share of exposures to clients in high-emitting sectors without credible transition plans

- Use both internal and external data sources, such as:

- Internal credit or portfolio analytics

- Outputs from climate scenario analysis

- External climate risk maps and data providers

- Expert judgment where data are limited

- Client disclosures and strategic plans

- Choose relevant key risk indicators (KRIs), such as:

- Validate and apply thresholds

- Risk, sustainability, business and internal audit teams should review proposed thresholds, testing them against past incidents where possible, and documenting insights from the calibration process.

- Materiality thresholds should be formally approved by the board.

- Once approved, thresholds should be communicated across the organisation and applied at relevant levels, such as portfolio, sector, segment or asset, and embedded in key processes including credit approval, portfolio monitoring and disclosure reporting.

- Review thresholds regularly, ideally on an annual cycle, and document any changes for future auditability.

Guidance 3c: Developing materiality thresholds

Guidance 3c presents practical examples of materiality indicators, thresholds and applications that can be used when setting climate risk boundaries. This framework helps to convert the institution’s risk appetite into clear, actionable triggers for monitoring and escalation.

CLICK TO VIEW Guidance 3C: Developing materiality thresholds.

Establishing escalation protocols

Clear escalation protocols can ensure climate risks identified within the risk appetite are managed consistently across the institution. By formalising reporting lines, assigning clear ownership and scheduling regular reviews, FIs can strengthen accountability, improve responsiveness and nurture a culture of continuous improvement.

- Define limits, triggers and thresholds

- (Developing and beyond) Include qualitative triggers such as identifying new or emerging material climate risks, or breaches of existing climate policies.

- (Advanced stage) Set specific, measurable thresholds on relevant KRIs, building on the materiality thresholds defined in the previous step.

- Map the escalation process across the three lines of defence

- (Embedded stage and beyond) Develop a process flow chart or table outlining:

- 1LoD (front-line lending officers) to screen risks where possible at origination. Responsibilities: Rapid climate risk screening (see Module 6).

- 2LoD (risk managers) act as operational risk and compliance guardrails. Responsibilities: Verify flagged risks, carry out further investigations and escalate issues to senior executives if needed.

- 3LoD (internal audit) ensure internal processes are fit for purpose. Responsibilities: Define the frequency and scope of internal audits, independently review key processes and decisions, and analyse incidents to recommend improvements.

- Oversight by designated committees to ensure accountability. Responsibilities: Prepare reporting templates, document key decisions and deliver recommendations for improvement into climate risk policy, governance framework and risk appetite.

- Specify reporting lines and responsible personnel for each step.

- (Embedded stage and beyond) Develop a process flow chart or table outlining:

- Establish action and remediation protocols

- (Embedded stage and beyond) Require clear action plans for all escalated risks, including assigned owners, deadlines, and follow-up monitoring.

- (Advanced stage) Mandate re-escalation if action plans are not completed or if similar incidents occur.

- Formalise decision-making authority

- (Developing stage) Specify which individuals or committees have authority to accept, mitigate or transfer escalated risks.

- (Advanced stage) Escalate material issues to relevant government bodies as required, and document all key decisions.

- Regular reporting and continuous improvement

- (Embedded stage and beyond) Develop dashboards or reporting templates to track threshold breaches, escalations and actions taken, with communication channels for rapid escalation, effective response and transparent documentation.

- (Developing stage and beyond) Conduct regular reviews, ideally annually, of escalation protocols, gather feedback and implement improvements to strengthen future processes.

Guidance 3d: Designing escalation protocols

Guidance 3d shows how FIs can put climate risk escalation protocols into practice, ensuring that risks are identified early, properly assessed and escalated to senior decision-makers when necessary.

CLICK TO VIEW Guidance 3d: Designing escalation protocols.